2019 Study: Compared to Boomers, Millennials’ Rent Is More Affordable — But They Can’t Afford Homes

Do millennials have it worse than past generations?

The popular narrative seems to suggest they do. Millennials have faced higher unemployment rates and higher student debt than past generations of young adults, according to a Pew Research Center report.

We compared these generations, following Pew’s definition of each, by looking at incomes and housing costs during the years their cohorts were entering independent adulthood and becoming financially established, 20 years after their birth years:

- Baby Boomers, born 1946 to 1964

- Generation X, born 1965 to 1980

- Millennials, born 1981 to 1996

Here’s what we found, and how it impacts millennials’ moving plans and habits.

Key Takeaways

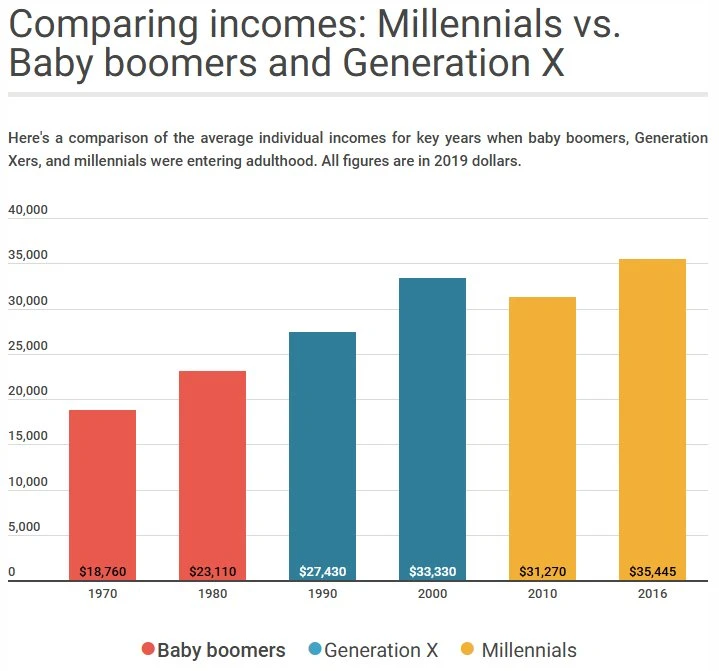

- The biggest generational jump in income was from baby boomers to Generation X. During the years each generation was entering adulthood, individual annual incomes grew by $6,180 from $21,250 for boomer to $28,590 for Generation X

- Thanks to the Great Recession, incomes didn’t grow as much from Gen X to millennials, incomes just $4,160 higher each year during the time millennials entered adulthood

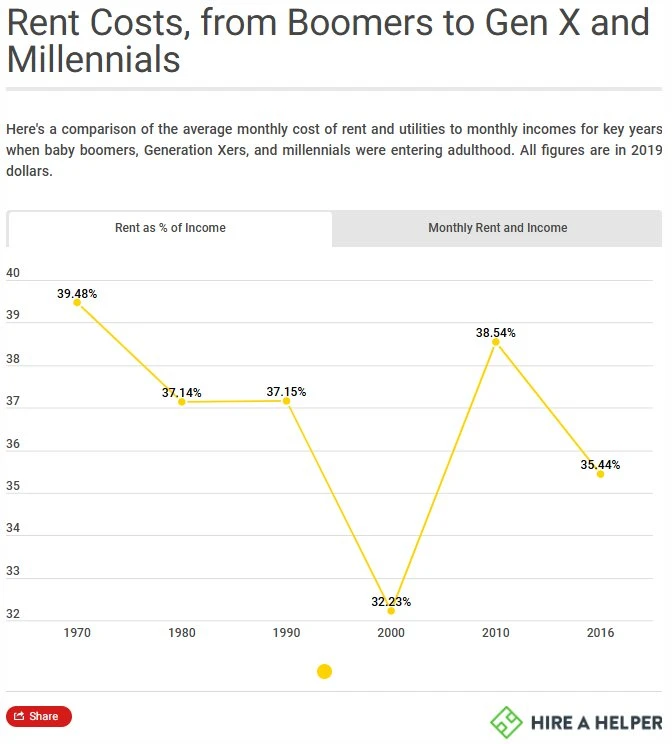

- Overall, baby boomers faced less affordable rent prices than Generation X or millennials. Over the years that boomers entered adulthood, the rent costs were equal to 38.1% of monthly incomes. This measure decreased to 35.9% for Gen X and 35.7% for millennials

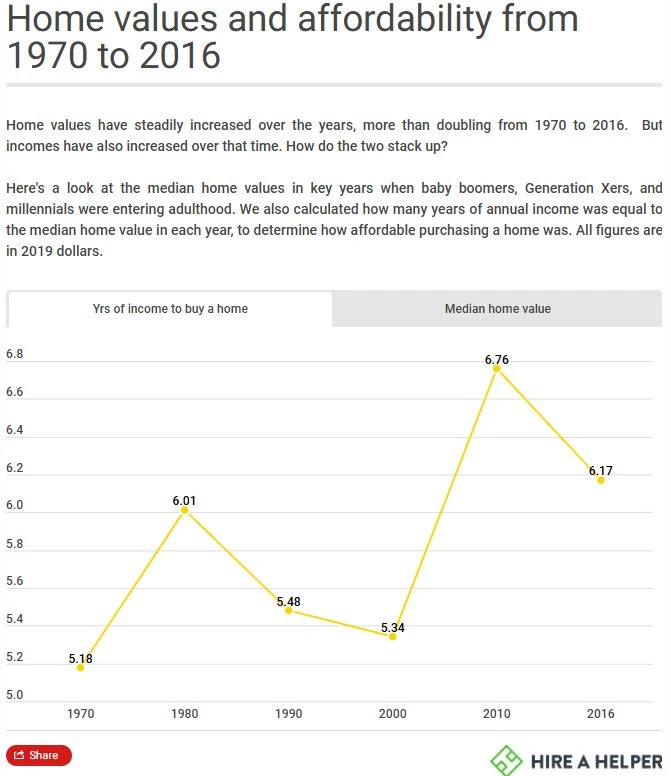

- Buying a home is still out of reach for many millennials. Millennials face home values that are higher and incomes aren’t keeping up. During their coming-of-age years, the average home was worth 6.4 years’ worth of income on average. That’s a 15% increase from the 5.6 years’ of income a typical home was worth, on average, for boomers and Gen Xers

Lauren Thomas

Lauren Thomas is the PR and Brand Marketing Manager at HireAHelper, where she leads all things brand, storytelling, and data journalism. With 9 years of experience across marketing copywriting, digital PR, and content marketing, she's built a career out of turning data and ideas into narratives people actually want to read.

She draws from years of experience in personal finance, insurance, and home services to help readers make smarter, more confident decisions about life's biggest expenses — moving included.

How Incomes Have Grown Since 1970

Compared to incomes in the years baby boomers and Gen Xers entered adulthood, incomes have grown during the years millennials have been adults. But these increases haven’t been without some stops and starts.

From 2000 to 2010, annual incomes fell by just over $2,000 (in 2019 dollars) following the downturn of the Great Recession. While incomes have recovered since then and risen by $4,771, millennials’ higher incomes have come with costs.

Specifically, these gains are due largely to millennials’ status as the most-educated U.S. generation to date. While earning these colleges degrees has helped this generation sustain income growth, it’s come with a cost: student debt. Millennials are twice as likely as members of Generation X to hold student debt, and owed 50% more on this debt, per Pew Research.

Rent Is Slightly More Affordable for Millennials, Compared to Boomers

During the years boomers entered adulthood from 1966 to 1984, a typical renter paid 38.1% of their income towards rent and utilities, on average. For a typical millennial entering adulthood, however, a smaller portion of monthly pay, 35.7%, was needed on average to cover rent and utilities from 2001 to 2016. For comparison, the same average for Gen Xers was 35.9%.

This overall trend shows that millennials generally faced rent costs that were about on par or slightly below what boomers would have paid at the same ages. But our data also shows differences even when comparing the youngest and oldest members of each generation.

Older millennials that entered adulthood in 2010 were putting more of their income toward rent at 38.5%, while younger millennials in 2016 paid just 35.4% of their income toward rent.

Older vs. younger boomers followed a similar trend. Older boomers paid rent costs equal to 39.5% of their monthly income in 1970. Younger members of this group had slightly more affordable rent, equal to 37.1% of monthly income in 1980.

Across the 15-16 year spans during which each generation was coming of age, however, millennials have generally benefited from slightly more affordable rent.

Here’s a look at how rent costs stacked up against incomes during the years that members of each generation were entering adulthood.

Buying a First Home Is More Costly for Millennials

While covering rent is potentially manageable, purchasing a home for the first time is a different story for millennials. This life milestone is further out of reach for them compared to young adults of past generations.

Fewer millennials own a home than Gen Xers or boomers at the same age, trailing these cohorts by about 8 percentage points according to The Urban Institute.

This is gap correlates with the findings of our analysis of home affordability for each generation. We went back to 1960 and compared U.S. Census Bureau data on home values to personal incomes during the years that baby boomers, Generation X, and millennials were entering financially independent adulthood.

Here’s an overview in 2019 dollars:

Home values and affordability from 1970 to 2017

Home values have steadily increased over the years, more than doubling from 1970 to 2017. But incomes have also increased over that time. How do the two stack up?

Here's a look at the median home values in key years when baby boomers, Generation Xers, and millennials were entering adulthood. We also calculated how many years of annual income was equal to the median home value in each year, to determine how affordable purchasing a home was. All figures are in 2019 dollars.

While both home values and incomes fluctuated for each generation, millennials are reaching adulthood at a time when buying a home is less affordable. Both boomers and Gen Xers would have had to pay around 5.6 times their annual pay for a first home, on average.

But housing costs relative to income are up 14.3% for millennials, compared to previous generations, with a typical home value equal to 6.4 years’ worth of individual income.

This shows that though incomes have grown and kept pace with earning benchmarks for past generations, house prices have risen faster. Other obstacles stand between millennials and their first home purchase: the burden of student debt, stricter home lending standards, and a shrinking supply of affordable housing. Overall, homeownership is far less accessible to millennials than it was to previous generations in their early years of adulthood.

Renting Is More Affordable Than Owning — But Comes With More Housing Insecurity

Overall, the answer to how millennials are faring when it comes to affording housing cost is mixed. Rents are as or slightly more affordable for millennials as they were for young adults in the boomer and Gen X cohorts.

But homeownership is less affordable, leaving fewer millennials able to graduate from renting to homeownership. The gap in affordability between owning a home and renting only seems to be widening, too, with 82% of renters viewing their current housing situation as more affordable than purchasing a home.

Homeownership Perks Millennial Renters Are Missing Out On

Because millennials can’t make the dollars and cents of buying a home add up, they’re also missing out on the many other benefits that owning a home provides. Homeownership is a key path to wealth accumulation for Americans, for example, as they build equity. And mortgages come with a tax break while renting doesn’t.

Perhaps just as important is that owning a home also provides more housing security, as it shields residents from the inherent unpredictability of renting.

While landlords can jack up rents each year, homeowners will only see increases when their property taxes are adjusted. If it rises too much, a renter might find themselves suddenly priced out of their home and forced to move to a cheaper place.

Depending on state rental laws, renters can also be evicted even if they’re model tenants. Common reasons renters might be evicted include if the unit is going to be completely remodeled, if the landlord wants to reclaim the property for their personal residency or use, or if they plan to sell it.

Renters’ living situations can even be complicated by their own living arrangements or personal lives. Couples who rent jointly but then split, for example, will be faced with navigating both a breakup and a move. Renters with roommates might be forced to move or become unable to afford rent if a roommate moves out or breaks the lease.

Whatever the situation, renters often have less control over their housing situations compared to their home owning peers.

Millennials Are Moving More Than Older Generations

These aren’t just possibilities, either — it’s happening. Past reports have pointed out that millennials are moving less than previous generations at the same age. But this could reflect an overall decline in move rates across generations.

A recent moving regrets survey from Porch (which owns HireAHelper), however, reveals that millennials are live in their homes for shorter periods and move more frequently than other generations.

Millennials report moving every two years, on average — twice as often as Gen Xers at four years, and three times more frequently than boomers who stay in a home for an average of six years. Additionally, three-quarters (73%) of millennials plan to move in the next 10 years, compared to just 58% of Gen Xers and 43% of boomers.

How Millennial Renters Can Prepare for Their Next Move

Millennial renters don’t have to be at the mercy of their landlords or the rental market. Looking ahead and preparing for future moves can lower the stress and costs of the whole ordeal. Here’s how to make your next move a smoother experience.

Know what’s in your lease. Your lease sets out the rules of you and your landlord’s agreement for you to rent your home. You should carefully read it and discuss any concerns before signing the lease, and review it occasionally to remember what’s in it.

Sticking to the agreements set out in the lease is crucial; if you break the lease, you might give your landlord the cause and legal right to evict you. Lastly, get familiar with your state’s tenant’s rights laws to know what is fair and legal treatment, and advocate for yourself if your landlord is overstepping.

Keep an eye on your rental market. If you stay up-to-date on overall trends in rentals for you area, you will be better informed about how these could affect you as a renter. You’ll see if rents are on the rise or if competition for units is up. You can also research neighborhoods beforehand so you know which areas offer rentals that fit your housing needs and budget.

Save a moving fund. Even if you’re given 30 days of notice to vacate, that’s not a lot of time to save up for a big move. You also might not be able to count on getting your rental deposit back before you’ll need to put money down on your next place. So, it’s wise to have enough savings that you can cover the full costs of a move including the moving van, movers, and the first month’s rent and deposit.

Declutter regularly. Moving will be easier and less stressful if you have less stuff you have to sort through, pack up, and relocate. So get in the habit of sorting through your belongings regularly, at least once per year. Be honest about whether you need, want, or use items, and donate or throw away things that no longer serve a purpose. This gives you a chance to reorganize your remaining stuff so that it’s easier to pack and move, too.

Make your moving plan. Don’t wait until you’re priced out of your apartment to start thinking about and planning your next move! You can review our moving checklist to get some ideas about what your move could look like.

Outline your own “moving cheat-sheet” that includes the steps you’ll need to take when moving. You can even include contact details for anyone you’ll need to contact when moving, such as your landlord, your bank, the post office, or the utilities company.

Know how to get help. Renters can’t always plan the move far in advance, which might make it difficult to plan and execute a move on your own. Hiring movers can make a huge difference in how stressful your move is, and HireAHelper can connect you with moving truck rentals, movers, and packers. A Hybrid Move covers the trickiest parts of the move: you pack up your belongings, and movers will load and unload the truck.

Methodology

HireAHelper analyzed Census Bureau data over the last 60 years to generate the intergenerational comparisons in this piece.

We followed generation definitions set by Pew, plus 20 years, to isolate the years that each generation was entering independent adulthood, as follows: Baby Boomers, born 1946 to 1964, entering adulthood from 1966 to 1984; Generation X, born 1965 to 1980, entering adulthood from 1985 to 2000; millennials, born 1981 to 1996, entering adulthood from 2001 to 2016.

For ease of understanding, all dollar amounts were converted into 2019 dollars. The census data used was from the Historical Census of Housing for home values and gross rents, for years from 1970 to 2000, and One-Year American Community Surveys by year reported, from years from 2001 to 2016.

Illustrations by Harry Woodgate

Latest Research

2025 Charlotte Moving Report

If it feels like everyone’s moving to Charlotte these days, you’re not imagining it! The Queen City is one of the fastest-growing places in North Carolina and the entire Southeast. According to our 2025 North Carolina Migration Report, 147 people move to Charlotte every day, part of a larger trend that has made North Carolina a top-five destination for movers nationwide. It’s drawing talent from across the state and beyond, reshaping how North Carolina grows and cementing its role as one of the country’s most dynamic cities.

We created this report to show what’s fueling that growth, who’s coming here, and what it means for people who already call Charlotte home.

The Future of Homeownership 2026

In 2026, the American Dream is facing a reality check. The median U.S. home price has climbed to $390,300 and is projected to reach $527,525 by 2031 - a 35.1% increase in just five years. But incomes aren't keeping up, despite growing minimum wages. Across the country, the gap between what people earn and what it takes to buy a home is widening fast, pushing homeownership further out of reach for millions of Americans.

This is a nationwide affordability crisis with sharp regional divides. In some states, buying a home still aligns with what the average household earns. In others, even an income of $100,000 falls short.

Using median home prices, household incomes, and five-year projections, this report reveals where Americans can still afford to buy today, where affordability is deteriorating fastest, and which markets may become realistic, or completely out of reach, by 2031.

2023 Study: 3 Million Moves Driven by Extreme Weather Events Last Year

In this study, HireAHelper takes a close look at moves forced by natural disasters in the United States.

Using the most recent data from the Census Bureau’s large-scale Household Pulse Survey and Current Population Survey, we focused on the number of disaster-forced moves over time, their typical destinations, as well as the types of disasters forcing most Americans out of their homes.

Study: How Much Does Moving Cost in 2023?

Driven by record inflation and rising fuel and vehicle costs, U.S. moving costs reached an all-time high in 2022. The average cost that year was $410—peaking at $454 in August—representing a 7% increase from 2021.

Prices have not yet given way; data from the first five months of 2023 shows an average moving cost of $399, which is 4% higher than the same period last year. It remains uncertain whether these costs will stay elevated or decline, which states will experience the sharpest price hikes, and if any areas will become cheaper.

2023 Study: Corporate Relocation at Highest Rate Since 2017

Whether to cut costs, gain a more beneficial tax rate, or be closer to a target market, about 9% of corporations in the United States moved their headquarters within the past fiscal year — the highest percentage since 2016-17, according to Securities and Exchange Commission (SEC) filings.

States like New York and cities like Seattle are seeing corporate headquarters move away, while smaller cities outside large urban centers are becoming new homes to big companies in tech and pharmaceuticals. Our study breaks down where companies are moving to, which states and cities they’re leaving behind, and whether workers are on board with following their employer to their new HQ location.

2023 Study: Where, How and Why Are Americans Moving This Year?

Every year, millions of Americans move, and over half (52%) of those moves take place during what we in the moving business call “moving season” — otherwise known as the summer months of May through August.

So what does the moving season hold for us this year? To get a sense of how many Americans intend to move, when they’re going to move, and what drives their moving decisions, HireAHelper conducted a nationally representative survey of 2,000 adults in the U.S. earlier this month.