Mortgage Affordability

Metropolitan Areas With The Best And Worst Affordability Indexes In 2019

December 4, 2019

To many Americans, the hurdles to homeownership can feel hopelessly daunting. Across wide swaths of the country, average families can't afford homes of their own without severely stretching their budgets. Many millennials find themselves sidelined from the housing market, struggling to save for down payments. And despite strong economic conditions, homeownership rates remain well below pre-recession levels.

Yet, the nation's homeownership prospects are not all doom and gloom. In many areas, home prices are so reasonable that mortgage payments consume just a fraction of household incomes. Elsewhere, typical mortgage payments are far less expensive than rents, making homeownership a wise fiscal move. You just need to know where to look – and where to steer clear of exorbitant home prices.

That's what this project is about. We identified the most and least affordable metropolitan areas nationwide, using data from Zillow to compare average mortgage payments to local household incomes. Where is homeownership in and out of reach across the country? Keep reading to find out.

Affording Ownership

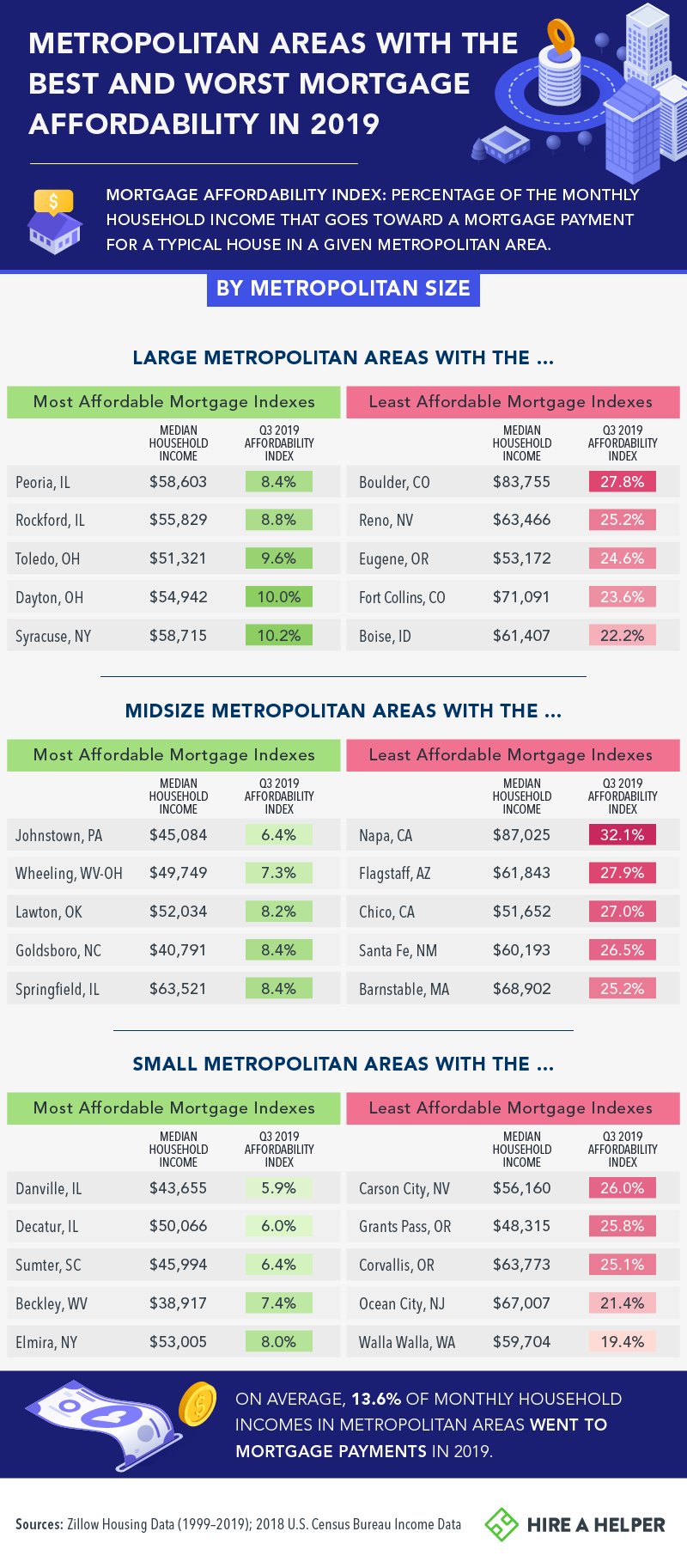

Housing affordability is a relative concept: Home prices are best assessed in relation to what local households are earning. The mortgage affordability index allows us to do that in each metropolitan area, gauging how much of the average household income a typical mortgage payment would consume. Nationwide, mortgage payments amounted to roughly 14% of monthly household earnings in 2019.

However, many cities offered far better deals. Among large metropolitan areas, two places in Illinois boasted the best affordability index figures: In Peoria and Rockford, mortgage payments consumed less than 9% of monthly household earnings.

Smaller metropolitan areas offered even better deals, even when local incomes were low. In Beckley, West Virginia, sometimes hailed as the nation's most affordable city, the affordability index was roughly 6% – despite having a median household income roughly $24,000 below the national average.

By contrast, the affordability index was nearly 28% in Boulder, Colorado, the nation's least affordable large metropolitan area. Housing prices in the mountainside city have reached critical levels, according to local officials, with the average single-family home selling for more than $1 million. In Reno, Nevada, the second-least affordable large metropolitan area, a dearth of affordable housing is driving public outcry. Smaller cities can also produce exorbitant home prices: In Napa, California, the nation's least affordable midsize metropolitan area, housing costs have driven away local workers.

Market Metamorphosis

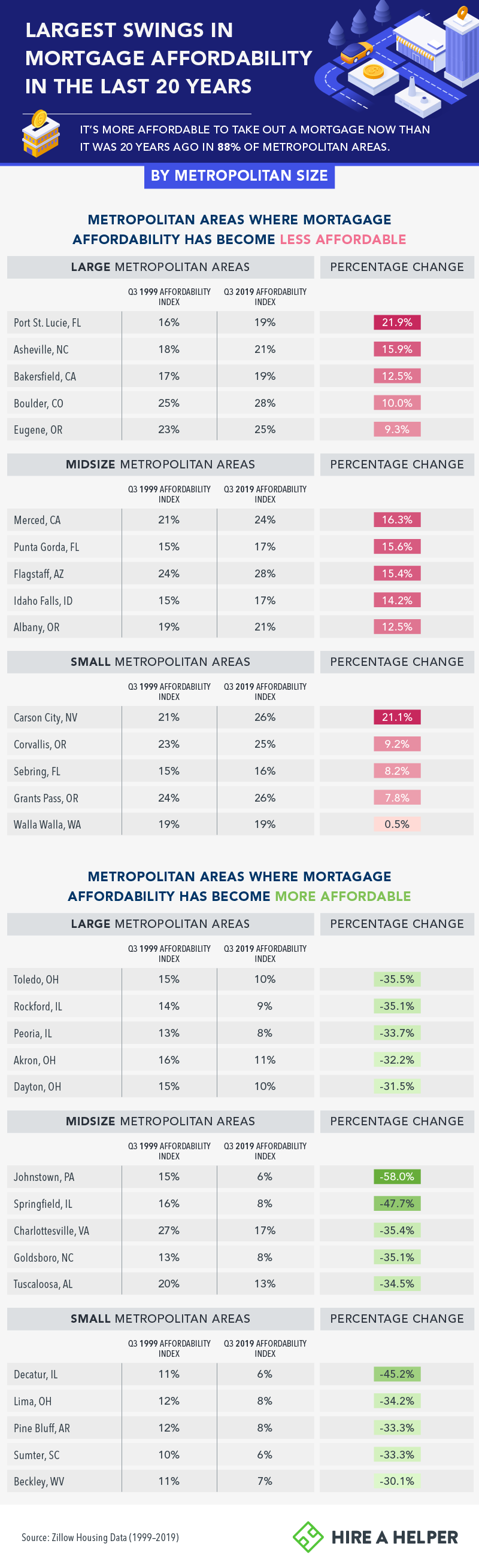

Many Americans bemoan rising housing costs, and home prices have soared in plenty of places. But these concerns obscure a more positive (and widespread) trend: Over the last two decades, mortgages have become more affordable in the majority of metropolitan areas. Indeed, while home prices haven't necessarily fallen, mortgage payments in most areas consume a smaller portion of household incomes than they did in 1999.

Take Johnstown, Pennsylvania, where typical mortgage payments amounted to 15% of monthly household incomes in 1999 – but just 6% in 2019. Decatur, Illinois, enjoyed a similar improvement in affordability, with a median home price of less than $90,000. Among large metropolitan areas, Toledo, Ohio, saw the most desirable change in affordability, although recent interest in the area may soon drive prices higher.

Unfortunately, certain metropolitan areas did see housing expenses grow immensely in relation to incomes. Port St. Lucie, Florida, where property values have recently surged, saw its affordability index figure rise from 16% to 19%. Among midsize metropolitan areas, Merced, California, saw the biggest affordability drop, thanks to a shortage of available housing.

Saving Money With a Mortgage?

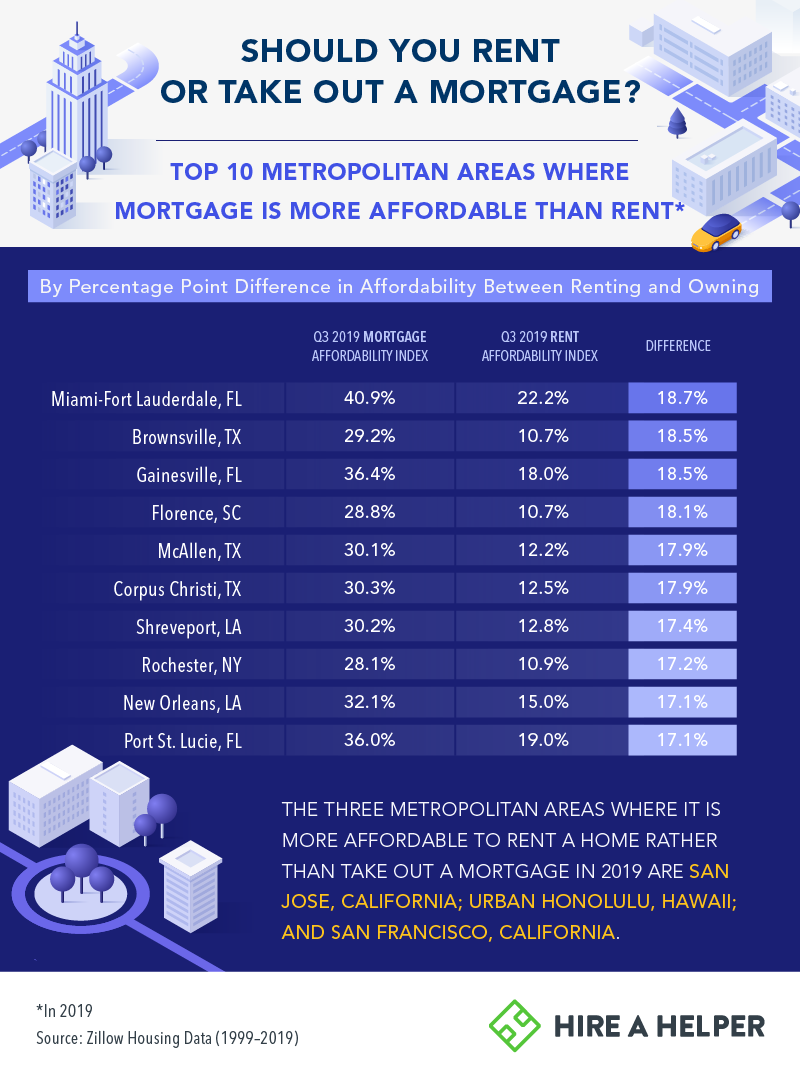

Owning a home can provide several long-term investment benefits, such as the ability to build equity and keep housing costs stable over time. But even on a monthly basis, mortgage payments tend to be less expensive than rent in many areas. This usually isn't the case in the nation's most costly housing markets, such as San Francisco and San Jose. But in plenty of cities large and small, rent significantly exceeded typical mortgage payments.

In the Miami-Fort Lauderdale metropolitan area, monthly rents were roughly 19 percentage points higher than the typical mortgage payment, although the influx of new rental units may soon stem rising rental prices. A similar gap emerged in Brownsville, Texas: Even though rental prices are notably low, mortgage payments were typically even less expensive.

A regional trend was clear: Most metropolitan areas in which mortgage payments were more affordable were located in the South. The exception to this rule was Rochester, New York, where the typical mortgage payment was 17 percentage points lower than the average rent. Although prices have recently risen in the city, the average home price remains well below $100,000, making Rochester an attractive location for real estate investors.

Moving On to Owning

Our results reveal the diversity of local housing markets: Within a single state, metropolitan areas can demonstrate totally different trajectories. And though affordable homes are scarce in many places, homeownership is increasingly affordable in other corners of the country. Additionally, even in places where mortgages are relatively expensive, owning costs less than renting on a monthly basis.

Accordingly, it's best to consider your own homeownership prospects in distinctly local terms. Don't be discouraged by headlines about the national housing picture. Instead, take the time to research possibilities that suit your financial circumstances, including areas you might not previously have considered. With some searching and saving, you might just find that owning a home is more attainable than you imagined.

If you do, we're here with the help you need to make that move. HireAHelper takes the uncertainty out of the moving process, allowing you to read reviews and compare prices for movers in your area. That means less stress about your stuff and more time to enjoy your new home.

Methodology and Limitations

Data for this study were sourced from Zillow's housing data portal. Housing data come from Q3 1999 through Q3 2019.

The mortgage affordability index is the percentage of the monthly household income that goes toward a mortgage payment for a typical house in a given metropolitan area.

We calculated where it is most significantly more affordable to take out a mortgage than to rent in 2019 by subtracting the rent affordability index by the mortgage affordability for every metropolitan area in Zillow's data.

Our data is dependent on the reporting and completeness of Zillow's database.

Fair Use Statement

Our findings illustrate that homeownership is achievable for many American families, so long as they know where to look. We hope you'll share our project as widely as possible, helping others understand their homeownership options. When you do share our results, please link back to this page so that others can review all our work. We also ask that you use our images and information strictly for noncommercial purposes.